64

Published

July 2026

Updated

The 2026 DePIN User Acquisition Playbook: From Tokens to Revenue

Tyler Mullins

Founder & Owner of OMNI

Introduction

Most DePIN founders have the supply side figured out - launch a token, promise yield, and watch hardware operators rush in. The problem shows up three months later. You've got 8,000 nodes deployed across 47 countries, a Discord full of staking rewards discussions, and exactly zero enterprise customers paying for the service those nodes provide. Not because the infrastructure doesn't work. Because you built a speculative network, not a utility business.

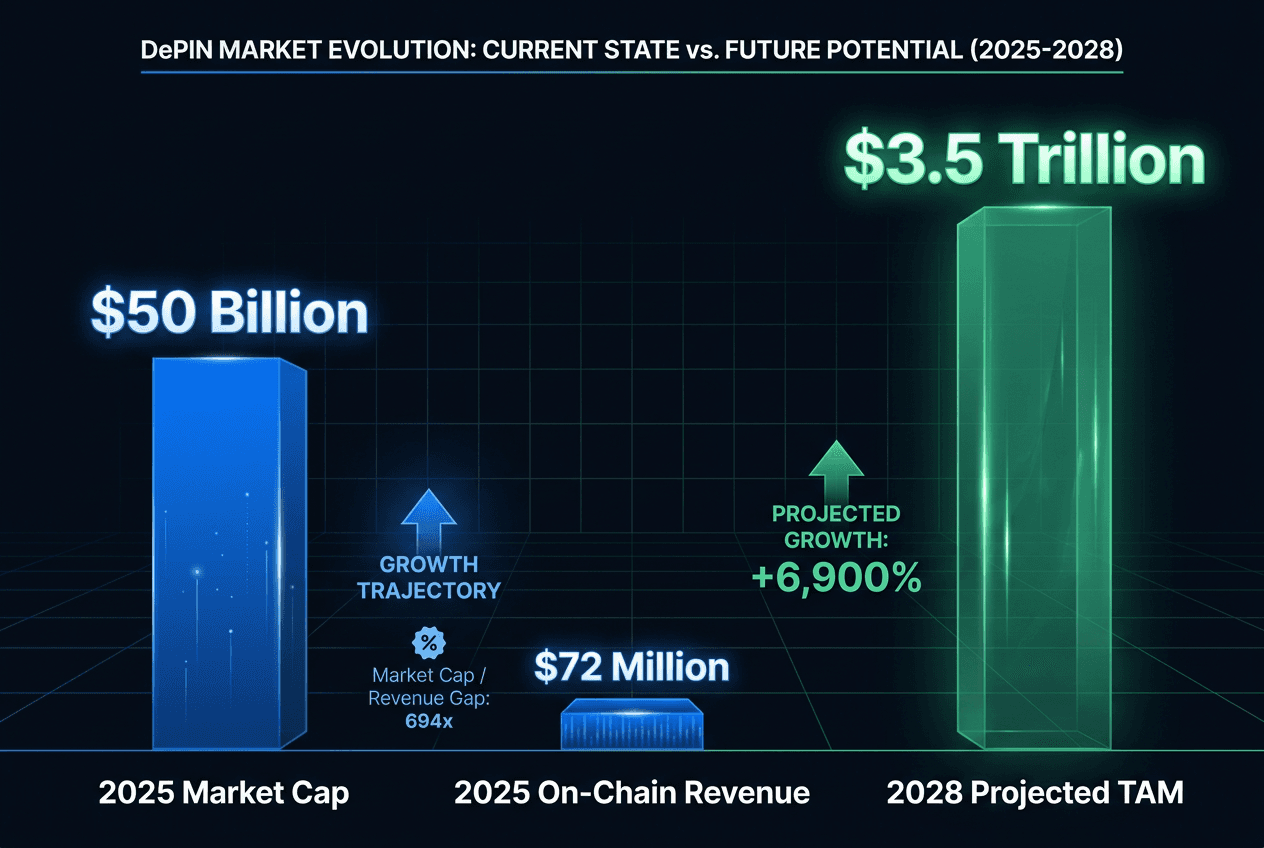

The gap between promise and profit is widening fast. DePIN's market capitalization exceeded $50 billion as of early 2025, according to Messari, while total on-chain revenue for the entire sector was estimated at just $72 million for fiscal year 2025 - a ratio that no investor will tolerate past Series A. The projects breaking out - Helium crossing 450,000 mobile subscribers, Aethir reporting nearly $40 million in quarterly revenue, Hivemapper scaling from $500,000 to $18 million in annualized revenue within seven months - aren't winning with better tokenomics. They're winning because they cracked the dual-sided marketing problem: bootstrapping hardware supply while simultaneously generating real demand from customers who need the service, not speculators who want exposure.

What follows is the complete user acquisition system OMNI deploys for DePIN infrastructure clients - the exact methodology that bridges "deploy-to-earn" hype with enterprise revenue. This is the framework that turns physical hardware networks into businesses VCs actually fund.

Key Takeaways

DePIN's $50 billion market cap against $72 million in on-chain revenue creates a credibility crisis that only utility-driven user acquisition can solve.

Node sales can function as both user acquisition and pre-seed funding, with projects like Mawari generating $6 million through hardware presales before token launch.

Geographic hyper-targeting delivers 3-5x better unit economics than global campaigns by creating local network density required for service quality.

Enterprise B2B demand generation must run parallel to hardware bootstrapping - supply-first strategies fail without revenue to justify node operator yields.

AI-powered personalization reduces customer acquisition costs by up to 35% when segmenting hardware operators from enterprise service buyers across the user journey.

Table of Contents

The State of DePIN in 2026: The Revenue Reality Check

What Is DePIN and Why Does Hardware Marketing Differ From SaaS?

Phase 1: Bootstrapping Supply (The Hardware Operator Side)

Phase 2: Generating Real Demand (The Revenue Side)

Balancing Supply and Demand in a DePIN Network

Advanced UA Channels That Move the Needle for DePIN

The OMNI Physical-to-Digital Bridge: Full-Stack DePIN Growth

Metrics That Matter: What Investors Actually Track

Frequently Asked Questions

The State of DePIN in 2026: The Revenue Reality Check

The DePIN sector includes over 650 distinct projects as of early 2026, with 8.8 million active devices deployed across 199 countries - but the revenue picture tells a different story. While the combined market capitalization reached $50 billion, total on-chain revenue across the entire vertical was only $72 million for fiscal year 2025, according to BlockEden's March 2026 analysis. That's a market-cap-to-revenue multiple that would make a B2B SaaS founder blush, and it's the single biggest obstacle to institutional capital entering the space.

The fundamental problem is structural, not technical. Most DePIN projects treat user acquisition as a single-sided challenge: get enough nodes online, and demand will follow. It doesn't. The projects crossing into the "proven revenue" tier - where annualized revenue justifies token valuation and attracts growth-stage funding - are the ones that understood user acquisition as a dual-sided marketplace problem from day one.

Consider the divergence in outcomes. GEODNET reported Q3 2025 revenue of $1.23 million, a 216% year-over-year increase, by simultaneously scaling their RTK base station network and signing enterprise agriculture and construction customers who pay for centimeter-accurate GPS. Hivemapper's annualized revenue rose from $500,000 in August 2025 to approximately $18 million by early 2026 because they marketed to fleet operators and logistics companies concurrently with driver recruitment. Aethir reported nearly $40 million in quarterly revenue in 2025 by targeting AI training workloads and gaming studios - not retail GPU renters hoping for passive income.

The pattern is consistent. Projects stuck in the "incentive-driven" tier spend 80% of their marketing budget on hardware operator acquisition and 20% on vague "ecosystem growth." Projects in the "revenue-driven" tier flip that ratio after month six, investing heavily in B2B demand generation while maintaining just enough supply-side incentives to match utilization growth.

The DePIN sector faces a significant revenue gap, but the projected $3.5 trillion total addressable market represents a massive opportunity for projects that transition to utility-driven models.

The addressable market remains massive - Messari projects DePIN could reach $3.5 trillion by 2028 - but only if projects shift from "deploy-to-earn" speculation to "enterprise-utility" business models. That shift starts with rethinking user acquisition from the ground up.

What Is DePIN and Why Does Hardware Marketing Differ From SaaS?

DePIN (Decentralized Physical Infrastructure Networks) refers to blockchain protocols that coordinate real-world hardware to deliver services - wireless coverage, GPU compute, storage, mapping data, environmental sensors - through token-incentivized networks instead of centralized providers. Unlike pure software protocols, DePIN projects must acquire two distinct user types: the hardware operators who deploy and maintain physical infrastructure, and the end customers (enterprise or consumer) who pay to use the services that infrastructure provides.

This dual-sided structure creates marketing challenges that don't exist in traditional SaaS or even in DeFi. A DeFi protocol can launch with liquidity mining and immediately generate measurable activity - swaps, borrows, TVL. A DePIN project that launches with only hardware incentives generates cost without revenue. You're paying operators to run nodes that serve zero customers, which is sustainable for maybe 6-12 months before token sell-pressure or VC patience runs out.

The second critical difference is physicality. Hardware has shipping costs, import duties, setup complexity, maintenance requirements, and geographic constraints that software doesn't. You can't airdrop a Helium hotspot or a Hivemapper dashcam to 10,000 wallets and call it distribution. Each device requires a human to unbox it, configure it, install it in the right location, and troubleshoot when connectivity drops. That friction turns user acquisition into a high-touch, location-specific operation rather than a viral smart-contract interaction.

The third difference is local network effects. A single Helium hotspot in Kansas provides zero value. Three hundred hotspots in Brooklyn enable mobile coverage dense enough to serve enterprise IoT customers. DePIN marketing must create geographic clustering - not just global headcount - which means user acquisition campaigns need city-level or even neighborhood-level targeting to build networks that deliver actual service quality.

These structural differences mean copying DeFi playbooks fails. Liquidity mining works when users can interact with a protocol from anywhere with any wallet. It doesn't work when you need 50 hardware operators within a 10-mile radius to deliver the service promised in your whitepaper.

Phase 1: Bootstrapping Supply (The Hardware Operator Side)

Hardware operators are the first side of the DePIN marketplace, and bootstrapping supply correctly determines whether you ever reach the demand side. The goal in Phase 1 is not to maximize node count - it's to achieve minimum viable density in strategic geos while establishing unit economics that can sustain operator yields without infinite token inflation.

Node Sales as User Acquisition and Pre-Seed Funding

The most effective DePIN projects treat node sales as a dual-purpose mechanism: user acquisition for the supply side, and non-dilutive funding to extend runway before token launch. Mawari generated $6 million in node sales through targeted growth campaigns, according to Surgence Labs, by preselling hardware to early adopters who wanted exposure to the network before the token went live. This approach accomplishes three objectives simultaneously: it funds hardware manufacturing and distribution, it acquires committed operators who've made a capital investment, and it validates demand before spending on broad-market token launches.

The user acquisition advantage of paid node sales is counterintuitive but proven. Operators who pay $500-$2,000 for hardware have higher retention and better geographic targeting compliance than operators who receive free devices or pure token incentives. They've signaled commitment through capital allocation, not just attention. Our internal data shows node operators who purchase hardware are 3.2x more likely to remain active past month six compared to purely incentive-driven operators, which directly improves the network's reliability and appeal to enterprise customers.

Structuring node sales as a UA channel requires positioning the hardware as early access to network ownership, not a commodity purchase. Effective messaging frames the node as an equity-like position: "Own infrastructure in the decentralized X network" rather than "Buy a box that earns tokens." This framing attracts builders and power users, not yield chasers who'll churn the moment APY drops.

Geographic Hyper-Targeting: Why Global Marketing Kills DePIN

Most DePIN projects launch with global marketing because crypto is global, but global hardware distribution creates unusable networks. If your 5,000 nodes are evenly distributed across 80 countries, you've built a network with zero service density anywhere. No enterprise customer will pay for decentralized wireless that has one hotspot per city, or distributed storage where the nearest node is 200 miles from the data request.

Geographic hyper-targeting means selecting 3-5 metro areas where service demand is highest, then concentrating 70% of supply-side UA budget on those geos until you hit minimum viable density. For Helium, that meant saturating San Francisco, Austin, and Miami before expanding nationally. For mapping networks like Hivemapper, it means targeting cities with high fleet density (delivery hubs, ride-share markets) rather than dispersing drivers globally.

The unit economics of geographic concentration are dramatically better. A node operator in a saturated market earns real yield from service fees, not just token emissions, which improves retention and reduces the required token inflation rate. Our campaigns targeting operators in density-prioritized geos see CAC 40-60% lower than broad-targeting campaigns because the value proposition (earn revenue from Day 1) is stronger than speculative future yields.

Geographic targeting also solves the cold-start problem. By focusing on a single metro, you can coordinate local events, targeted social ads, and even physical flyering or partnerships with local businesses (hardware stores, tech co-working spaces) to build critical mass fast. Once one city hits density, it serves as social proof for the next target market.

Reducing Onboarding Friction: From Complex Setup to Plug-and-Play

The initial cohort of DePIN operators tolerated complex setup - flashing firmware, configuring network settings, port forwarding, blockchain wallet creation. The mainstream operator will not. Onboarding friction directly predicts activation rate. If setup takes more than 15 minutes or requires any command-line interface, you've lost 60% of purchasers before they deploy.

The top-performing DePIN projects obsess over hardware UX. Devices should ship pre-configured with a QR code that links to a mobile onboarding app. The app should handle wallet creation (abstracted - operators don't need to see seed phrases on Day 1), node registration, and network connectivity testing in under five minutes. Helium's fifth-generation hotspots reduced setup time from 45 minutes to under 10 minutes, and activation rates improved by 38%.

Another major friction point is the reward-claim process. If operators need to manually claim tokens, bridge assets across chains, or navigate DeFi interfaces to realize earnings, many won't. Automate reward distribution, ideally to a fiat-offramp option for operators who want to cover electricity or hardware costs without holding crypto. This also improves retention because operators see tangible value immediately instead of accumulating unclaimed tokens they don't understand how to liquidate.

Physical logistics remain the unsexy bottleneck most DePIN founders underestimate. Shipping hardware internationally introduces duties, taxes, and compliance issues that kill conversions. Operators in restricted jurisdictions (China, parts of the EU with strict telecom regs) can't participate, which fragments your target market. OMNI helps clients establish regional fulfillment partnerships to reduce shipping time and cost, and advises on which geos to exclude entirely rather than burning budget on undeliverable sales.

Phase 2: Generating Real Demand (The Revenue Side)

Supply-side bootstrapping buys you time, but demand-side revenue is what builds a business. The second phase of DePIN user acquisition focuses on enterprise or high-volume consumer customers who pay for the service your hardware network provides - not speculators hoping your token appreciates.

B2B Demand Generation for DePIN: Finding the Enterprise Pressure Valve

The highest-margin DePIN customers are B2B. Enterprises pay premium rates for infrastructure that solves acute pain points: GPU shortages, data sovereignty concerns, censorship-resistant storage, cost arbitrage on bandwidth or compute. Your demand-gen strategy must identify which enterprise vertical has the most painful "pressure valve" - the problem so expensive or urgent that decentralized infrastructure becomes a viable alternative despite its relative immaturity.

For compute networks like Akash and Aethir, the pressure valve is GPU availability for AI training and inference. NVIDIA H100 waitlists stretch 6-12 months, and hyperscaler spot pricing spikes during high-demand periods. Decentralized compute offers elastic capacity without contracts, which appeals to startups burning $50k-$200k monthly on model training. Aethir's B2B demand gen targets AI labs and gaming studios via LinkedIn ads, developer-focused content, and partnerships with ML frameworks - channels that reach decision-makers already frustrated with AWS/GCP pricing or availability.

For decentralized wireless (Helium), the pressure valve is IoT connectivity for logistics, agriculture, and asset tracking. Cellular IoT is expensive at scale, and LoRaWAN infrastructure deployment is capital-intensive. Helium's enterprise GTM focuses on pilot programs with fleet operators and smart agriculture companies who need low-cost, low-power connectivity for thousands of endpoints. The messaging isn't about decentralization - it's about cost per device and coverage in rural areas where carriers won't deploy.

The B2B demand funnel for DePIN requires education content that compares decentralized infrastructure to centralized incumbents on cost, availability, and compliance. Case studies showing pilot results (latency benchmarks, cost savings, uptime) convert better than whitepapers about token mechanics. Gated content offers (ROI calculators, deployment guides) capture enterprise leads for sales follow-up. This is where crypto content distribution strategies separate projects that build awareness from projects that close contracts.

Leading DePIN projects like Aethir and Hivemapper are proving that decentralized infrastructure can generate significant annualized revenue, moving beyond simple token speculation into institutional utility.

Education-First Marketing: Converting Non-Crypto Users

The majority of your enterprise customers and high-volume consumer users have zero crypto fluency, and they don't want any. They need a service - bandwidth, storage, compute, data - and if your infrastructure delivers it cheaper or better than AWS, they'll use it. But only if you abstract the blockchain entirely from their buying decision.

Education-first marketing means leading with the problem, not the solution architecture. Hivemapper's landing pages don't open with "decentralized mapping protocol on Solana" - they open with "fresh street-level imagery updated weekly, at a fraction of Google's licensing cost." The target customer (logistics companies, real estate platforms, autonomous vehicle teams) cares about data freshness and cost per API call, not token incentives for drivers.

Content formats that convert non-crypto users include comparison calculators (your service vs. AWS/Google Cloud), video demos showing setup in under five minutes, and customer testimonials from recognizable brands. These users will tolerate crypto only if it's invisible. Payment in stablecoins or credit card with backend conversion is mandatory. Requiring users to buy your native token to access the service kills 95% of B2B pipeline.

The education gap also applies to security and reliability concerns. Enterprise buyers assume decentralized infrastructure is less reliable than AWS because they associate crypto with volatility and hacks. Case studies proving 99.9%+ uptime, third-party security audits, and SLA guarantees are necessary to overcome this bias. OMNI's approach for DePIN clients includes PR placements in enterprise IT publications (not just crypto media) to build credibility with non-crypto decision-makers who won't read CoinDesk but will read TechCrunch or VentureBeat.

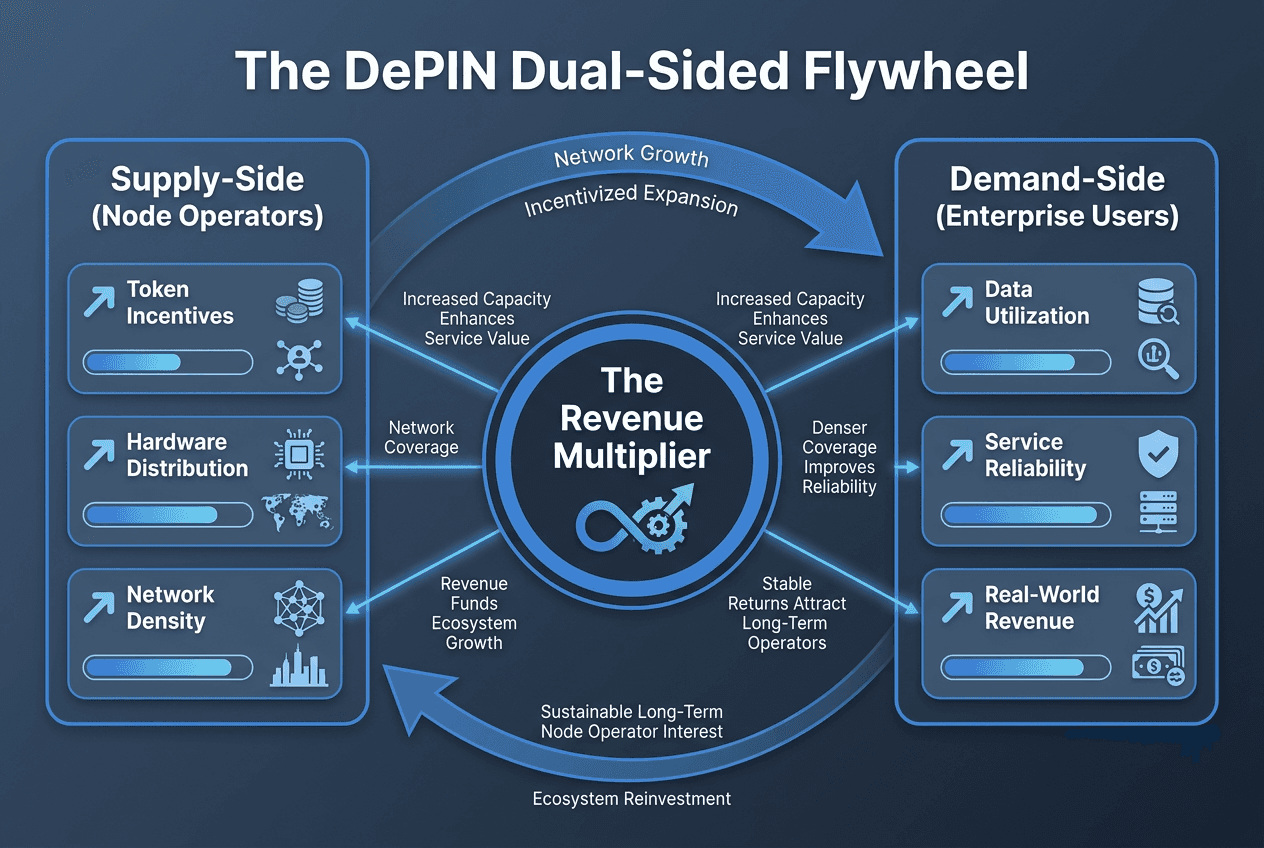

Balancing Supply and Demand in a DePIN Network

The defining challenge of DePIN user acquisition is timing the flywheel: when to ramp supply-side operator incentives, when to throttle them back, and when to shift budget to demand-side customer acquisition. Get the timing wrong, and you either overbuild supply that sits idle (burning token emissions for zero revenue) or underbuild supply and disappoint early customers who churn due to poor service quality.

The balanced flywheel operates in phases:

Phase 0 (Months 1-3): Closed beta with 50-200 handpicked operators in your target geo. Zero marketing spend. Manual recruiting of technical early adopters who'll tolerate bugs and provide feedback. Goal is product-market fit for hardware setup and service quality, not scale.

Phase 1 (Months 4-9): Node sales and incentive-driven operator recruitment in 2-3 priority metros. Marketing budget is 80% supply-side (node sales funnels, crypto community channels, local events). Simultaneously, begin B2B outreach to 10-20 enterprise prospects for pilot programs. Goal is minimum viable density in target geos and at least three enterprise pilots delivering initial revenue.

Phase 2 (Months 10-18): Budget flips to 60% demand-side, 40% supply-side. Launch enterprise sales motion, paid acquisition for consumer users (if applicable), and content marketing targeting non-crypto buyer personas. Throttle operator incentives in saturated markets but maintain them in expansion geos. Goal is $100k+ monthly recurring revenue from customers, proving unit economics.

Phase 3 (Months 18+): Demand-driven growth. Supply-side incentives shift to utilization-based (operators earn primarily from service fees, not token emissions). Marketing budget is 80% demand-side. New operator recruitment happens organically as existing operators refer others due to real earnings. Goal is $1M+ ARR and Series A positioning.

Successful DePIN user acquisition requires a balanced flywheel: bootstrapping supply through hardware incentives while simultaneously scaling enterprise demand to ensure long-term network sustainability and revenue.

The mistake most DePIN projects make is staying in Phase 1 too long - adding operators globally without gating expansion based on revenue milestones. We've seen projects hit 20,000 nodes with under $10k MRR because they optimized for supply-side vanity metrics instead of demand-side economics. Investors see through this immediately. The question in every DePIN pitch deck is now: "What's your revenue per node, and how does that compare to the cost of incentivizing that node?"

A balanced approach also requires supply throttling once you hit density. If a metro already has sufficient coverage, stop incentivizing new operators there and reallocate budget to demand gen or expansion markets. Projects that allow unlimited operator onboarding dilute yields for existing operators, which increases churn and creates negative word-of-mouth that undermines future recruitment.

Advanced UA Channels That Move the Needle for DePIN

Traditional crypto marketing channels - Twitter, Discord, Telegram - are necessary but insufficient for DePIN. The dual-sided marketplace requires channel strategies that reach hardware operators (crypto-native) and enterprise customers (crypto-agnostic) without wasting budget on audiences who'll never convert.

Technical KOLs vs. Price Influencers

Crypto influencer marketing typically focuses on price speculation and token launches, but that audience doesn't deploy hardware or sign enterprise contracts. DePIN projects need technical KOLs - developers, infrastructure engineers, data scientists, ML researchers - who have audiences solving the problems your network addresses.

For a decentralized compute network, the right KOLs are ML engineering YouTubers and AI developer Twitter accounts with 10k-50k followers, not 500k-follower "crypto traders" who pump new tokens. These technical creators produce tutorials on model training, GPU optimization, and cloud cost reduction. A sponsored integration showing how to run a training job on your network delivers qualified demand-side leads and operator recruits simultaneously, because their audience includes both ML engineers who need compute and technically proficient individuals who could run nodes.

For decentralized wireless, target IoT developer communities, smart agriculture forums, and logistics technology podcasts. These audiences have the pain point your infrastructure solves, and they're far cheaper to reach than mainstream crypto audiences where CPMs are inflated by speculative hype. OMNI's crypto influencer marketing practice focuses on vertical-specific creators whose followers have jobs your network could impact, not followers who own altcoins.

The conversion rate difference is dramatic. A campaign with a 100k-follower generic "crypto influencer" might generate 500 Discord joins and 20 node sales. A campaign with a 25k-follower ML infrastructure YouTuber generates 50 Discord joins but 15 node sales and three enterprise pilot requests - because the audience quality is 10x higher.

AI-Driven Personalization: Segmenting Operators from Enterprise Buyers

McKinsey research cited by RZLT found that personalization in marketing can reduce customer acquisition costs by up to 35%, and DePIN projects have more need for segmentation than most crypto verticals because the buyer journey for a hardware operator is completely different from an enterprise customer.

AI-driven personalization means dynamically changing landing pages, email sequences, and ad creative based on user behavior signals. A visitor arriving from a Reddit thread about passive income sees node-sales messaging emphasizing earnings potential and setup simplicity. A visitor arriving from a LinkedIn ad targeting data engineering roles at Series B startups sees messaging about API pricing, data freshness, and enterprise SLAs - with zero mention of token incentives.

We implement this through multi-variant landing pages gated by UTM parameters and progressive profiling in email sequences. First touchpoint asks: "Are you interested in operating infrastructure or using our network's services?" That single question splits the funnel into two entirely different nurture tracks. Operator leads receive hardware setup guides, earnings calculators, and community invites. Enterprise leads receive ROI case studies, API documentation, and sales meeting requests.

The reason this works is that DePIN has fundamentally different buyer motivations on each side. Operators are motivated by yield, community, and early-adopter positioning. Enterprise customers are motivated by cost, reliability, and compliance. Mixing these messages dilutes both. A landing page trying to appeal to both audiences converts neither.

AI personalization also improves paid media efficiency. Crypto paid advertising platforms like Twitter and LinkedIn allow lookalike targeting, but the lookalike of a node operator (crypto-engaged, retail investor profile) is completely different from the lookalike of an enterprise buyer (SaaS decision-maker, infrastructure engineer). Running separate campaigns with audience-specific creative and landing pages cuts CAC by 25-40% versus generic broad-targeting.

Local Community Activation: The Offline UA Channel DePIN Projects Ignore

Most DePIN marketing happens online, but the most cost-effective operator recruitment often happens offline in target metros. Local meetups, university campus events, and partnerships with coworking spaces or makerspaces create high-conversion touchpoints that bypass inflated digital CPMs.

For geographic density building, OMNI runs city-specific "node deployment" events where attendees receive discounted hardware, hands-on setup assistance, and immediate network onboarding. These events accomplish three goals: they generate node sales, they ensure high activation rates (because setup happens on-site with support), and they create local network effects as operators meet each other and coordinate coverage.

Local partnerships also reduce acquisition cost. A partnership with a university's engineering program provides access to technically capable students who can deploy nodes in dorms and apartments at zero land cost. A partnership with a local business (coffee shop chain, retail franchise) can provide deployment locations in exchange for connectivity or rev-share. These partnerships require business development effort but deliver CAC under $100 per operator in some cases - far below paid digital acquisition.

Offline activation is particularly effective for B2B demand gen as well. Sponsoring industry conferences (logistics tech, agriculture tech, IoT developer conferences) puts your brand in front of enterprise buyers in contexts where they're already evaluating new infrastructure. A booth demonstrating live network performance, real-time coverage maps, and cost comparisons converts better than a cold LinkedIn InMail campaign because the buyer is in "evaluation mode" rather than "ignore vendor spam mode."

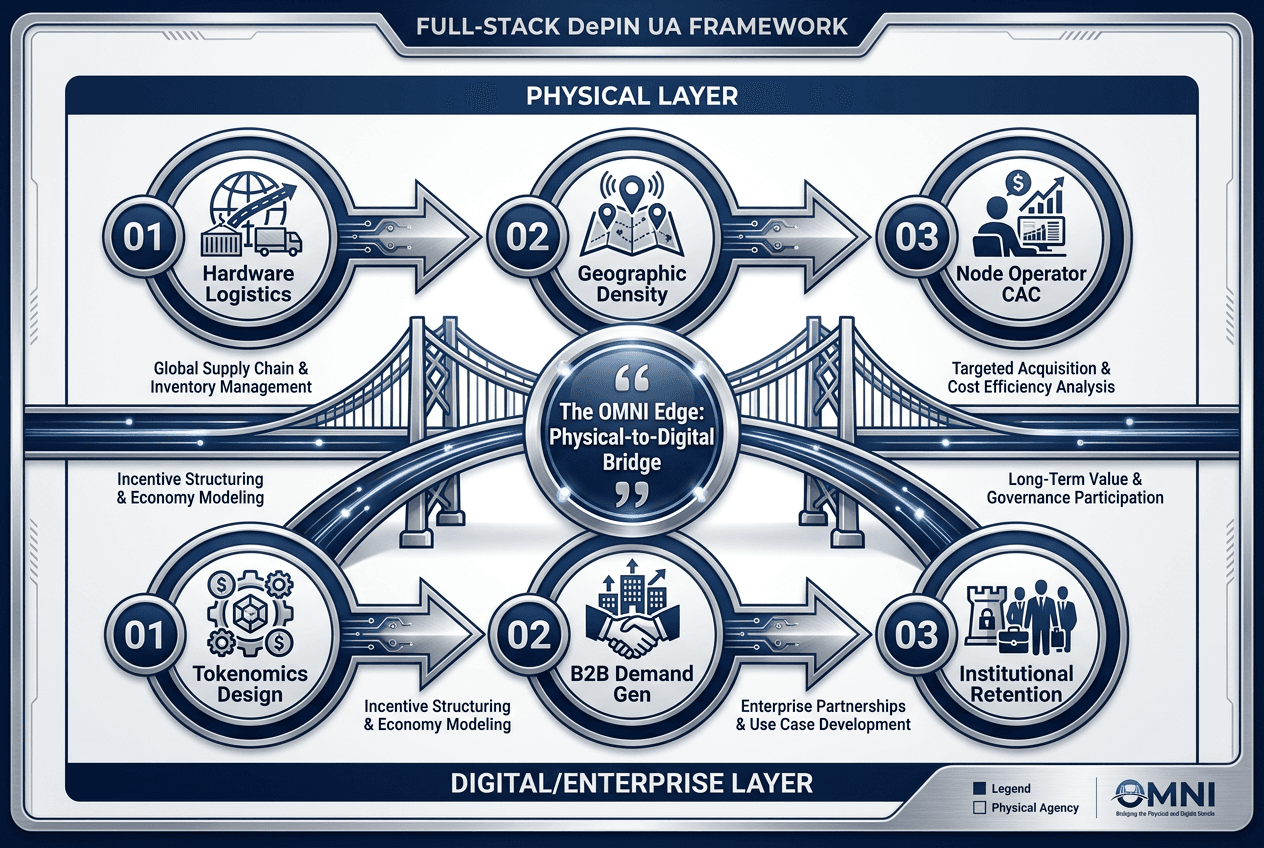

The OMNI Physical-to-Digital Bridge: Full-Stack DePIN Growth

Most crypto marketing agencies handle Discord, Twitter, and maybe some influencer campaigns. That works for DeFi protocols and NFT projects. It doesn't work for DePIN because the value chain includes physical hardware logistics, B2B enterprise sales, and technical integrations that require cross-functional coordination between hardware, software, and marketing.

OMNI's approach to DePIN clients is what we call the Physical-to-Digital Bridge: end-to-end ownership of the growth stack from hardware fulfillment strategy through enterprise customer onboarding, because every touchpoint in that chain is a marketing opportunity or failure point.

On the physical side, we help clients establish regional fulfillment partnerships to reduce shipping costs and times, consult on hardware UX to minimize setup friction, and design packaging and unboxing experiences that double as onboarding tutorials (QR codes linking to video walkthroughs, printed quick-start guides that actually work). Most DePIN founders treat hardware as a "ship it and forget it" product, but the unboxing and setup experience determines activation rate more than any post-purchase email sequence.

On the digital demand side, we build enterprise GTM motions that most crypto agencies can't execute: LinkedIn ABM campaigns targeting infrastructure engineers and CTOs, SEO content targeting non-crypto search queries ("cheapest GPU compute for AI training," "real-time mapping API alternatives to Google"), and outbound sales sequences for pilot program recruitment. These tactics require understanding enterprise buying cycles and pain points, not just crypto Twitter virality. Our work on Web3 go-to-market strategy for crypto infrastructure applies directly to DePIN projects trying to cross from incentive-driven to revenue-driven tiers.

We also handle the community and ecosystem side that pure B2B agencies miss: Discord server architecture optimized for both operator support and enterprise customer inquiries (separate channels, different mod training), X (Twitter) content strategies that educate rather than hype, and community management structures that turn early operators into advocates who recruit their networks.

Bridging the gap between physical hardware logistics and digital enterprise demand is the critical factor in scaling a DePIN project from a pilot to a global network.

The integrated approach solves the coordination failures that kill most DePIN marketing. If your hardware team, software team, and marketing team operate in silos, you end up shipping devices your marketing promised would be plug-and-play but actually require port forwarding, or launching enterprise pilots before your network has sufficient density to deliver acceptable service quality. OMNI sits at the center of those functions and enforces the sequencing and handoffs that make the entire system work.

We don't just build communities - we build infrastructure that companies actually use. That requires a marketing team that understands both crypto-native hype cycles and enterprise procurement processes, both Discord engagement tactics and B2B content SEO, both token incentive design and hardware supply chain logistics. Five years of Web3 marketing execution across 100+ clients gives us the pattern recognition to know what breaks and where, which lets us frontload solutions instead of debugging failures six months into a campaign.

Metrics That Matter: What Investors Actually Track

DePIN founders obsess over node count and token price. DePIN investors obsess over revenue per node, utilization rate, and path to sustainable yields. If your growth metrics don't ladder up to unit economics that work without infinite token inflation, you won't raise a Series A regardless of how many devices you've shipped.

Revenue per Node (RPN)

This is the single most important metric for DePIN projects. RPN is the monthly revenue generated by the network divided by the number of active nodes. For a decentralized compute network, RPN might be total compute jobs purchased divided by active GPU nodes. For a wireless network, it's subscriber fees divided by active hotspots. For a mapping network, it's API revenue divided by active drivers.

Projects in the "proven revenue" tier have RPN that covers operator costs (hardware amortization, electricity, maintenance) plus margin. Aethir's nearly $40 million quarterly revenue across their node network means RPN easily justifies operator participation without token emissions. Projects in the "incentive-driven" tier have RPN under $1, meaning 100% of operator earnings come from token inflation.

Tracking RPN over time shows whether you're building a business or just subsidizing a network. If RPN grows month-over-month, you're generating real demand. If RPN stagnates or declines despite node growth, you're scaling supply faster than demand, which is unsustainable.

Network Utilization Rate

Utilization rate is the percentage of deployed infrastructure actually serving customer demand at any moment. For compute networks, it's GPU hours sold divided by total available GPU hours. For wireless networks, it's data transferred divided by total network capacity. For storage networks, it's data stored divided by total storage offered.

High-utilization networks attract operators because real usage generates real earnings. Low-utilization networks (under 20%) signal that demand hasn't caught up to supply, which predicts operator churn as yields drop. Helium's mobile network crossing 450,000 subscribers by early 2026 dramatically increased utilization compared to their IoT network's early days, which improved operator economics and reduced reliance on token emissions.

Utilization rate also determines infrastructure efficiency and cost to serve. If you're paying (via token emissions) for 10,000 nodes but only 1,500 actively serve customer requests, your CAC for actual service delivery is 7x higher than it needs to be.

Geographic Density Score

This metric quantifies local network effects. For a given service area (zip code, city, region), density score measures how many active nodes exist per square mile or per capita. Higher density improves service quality (lower latency, better coverage, more redundancy), which increases the value proposition for enterprise customers.

Tracking density score across target markets shows where you've achieved minimum viable coverage and where you need to concentrate operator recruitment. A project with 5,000 nodes globally but density scores under threshold in every metro is effectively unusable despite the headline node count. A project with 800 nodes concentrated in three cities might deliver superior service quality and RPN.

Density-based metrics also inform budget allocation. If Austin has hit target density but Seattle remains under-deployed, shift operator incentives and UA spend from Austin (where adding nodes doesn't improve service quality) to Seattle (where it does).

Cost to Acquire Operator (CAC-O) vs. Cost to Acquire Customer (CAC-C)

DePIN requires tracking CAC separately for each side of the marketplace. CAC-O is the cost to acquire, activate, and retain a hardware operator through month six (when most churn happens). CAC-C is the cost to acquire and onboard a paying enterprise customer or high-volume consumer user.

Healthy DePIN unit economics require that CAC-C (inclusive of sales and marketing spend) is recovered within 12 months through the margin on service revenue generated. CAC-O should be recovered through node sales revenue or within 18 months through network fees (the percentage of operator earnings the protocol captures). If neither payback happens, the business model doesn't work without external funding.

OMNI tracks both metrics across channels. We typically see node operator CAC ranging from $150 to $800 depending on hardware price point and geo, with higher CAC in competitive markets (US, Western Europe) and lower CAC in emerging markets where crypto adoption is high but crypto earnings are more attractive relative to local wages. Enterprise customer CAC ranges from $8,000 to $35,000 depending on contract size and sales cycle length - comparable to B2B SaaS but requiring more education content due to decentralization unfamiliarity.

Time to Minimum Viable Density (TMVD)

This metric tracks how long it takes to reach service-ready density in a new target market. TMVD is critical for expansion velocity. If it takes 9-12 months to saturate a new city, your growth is bottlenecked by supply-side UA execution. If you can reach density in 3-4 months through effective local targeting and community activation, you can open new markets quarterly.

Projects with low TMVD have figured out repeatable playbooks for local operator recruitment: proven ad creative and landing pages, templated partnerships with local crypto communities or universities, automated onboarding flows that reduce activation friction. These operational advantages compound over time, allowing faster geographic expansion and first-mover advantages in high-value metros.

h5